Market Spotlight

August 27, 2025 |

Download

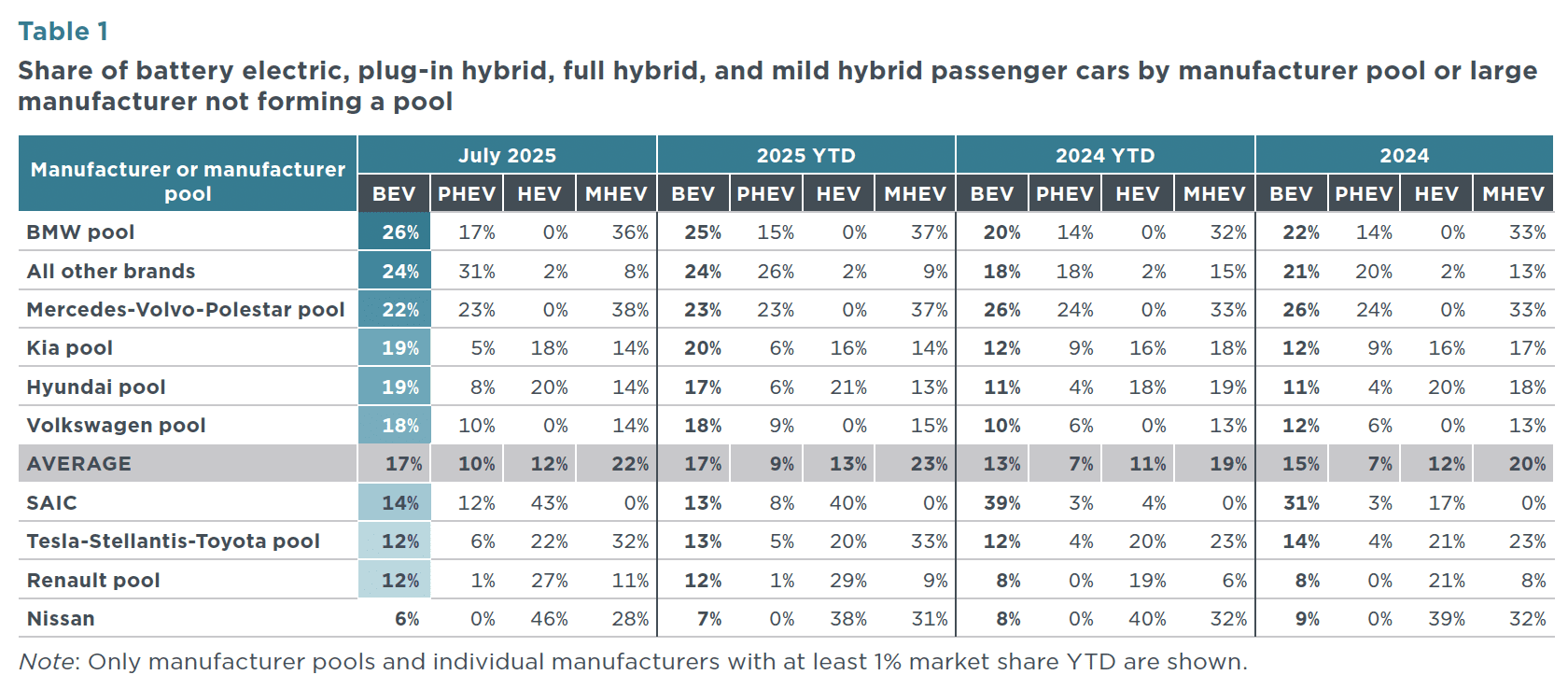

The average share of battery electric vehicles (BEVs) among total new registrations in Europe fell to 17% in July 2025, down from 18% in June. Year–to–date (YTD) 2025, the BEV registration share remained stable at 17%, which represents an increase of 4 percentage points compared with the same period of 2024. Several manufacturing pools had significant increases in BEV shares in 2025 YTD compared with the same period in 2024. Kia (20%) and Volkswagen (18%) both recorded increases of 8 percentage points, while BEV shares for the BMW (25%) and Hyundai (17%) pools increased 5 and 6 percentage points, respectively. In contrast, SAIC BEV registration share dropped to 13% in 2025 YTD from 39% over the same period of 2024. In July 2025, the BMW pool led with a 26% registration share, followed by the Mercedes-Volvo-Polestar (22%), Kia (19%), Hyundai (19%), and Volkswagen (18%) pools. Manufacturers with BEV registration shares below the European average were SAIC (14%), the Tesla-Stellantis-Toyota pool (12%), the Renault pool (12%), and Nissan (6%).

Compared with the previous month, manufacturer-level BEV shares in July 2025 were largely stable, except for the Tesla-Stellantis-Toyota pool and SAIC shares, which fell by 5 and 4 percentage points, respectively. Plug-in hybrid electric vehicles (PHEVs) had an average market share among new registrations in Europe of 9% in the first seven months of 2025 (up 2 percentage points over 2024 YTD), led by the Mercedes-Volvo-Polestar pool (23% share). For full hybrid electric vehicles (HEVs), SAIC (40%) and Nissan (38%) recorded the largest shares in 2025 YTD. In the mild hybrid electric (MHEV) segment, the BMW and Mercedes-Volvo-Polestar pools led registration shares, each with a 37% in 2025 YTD.

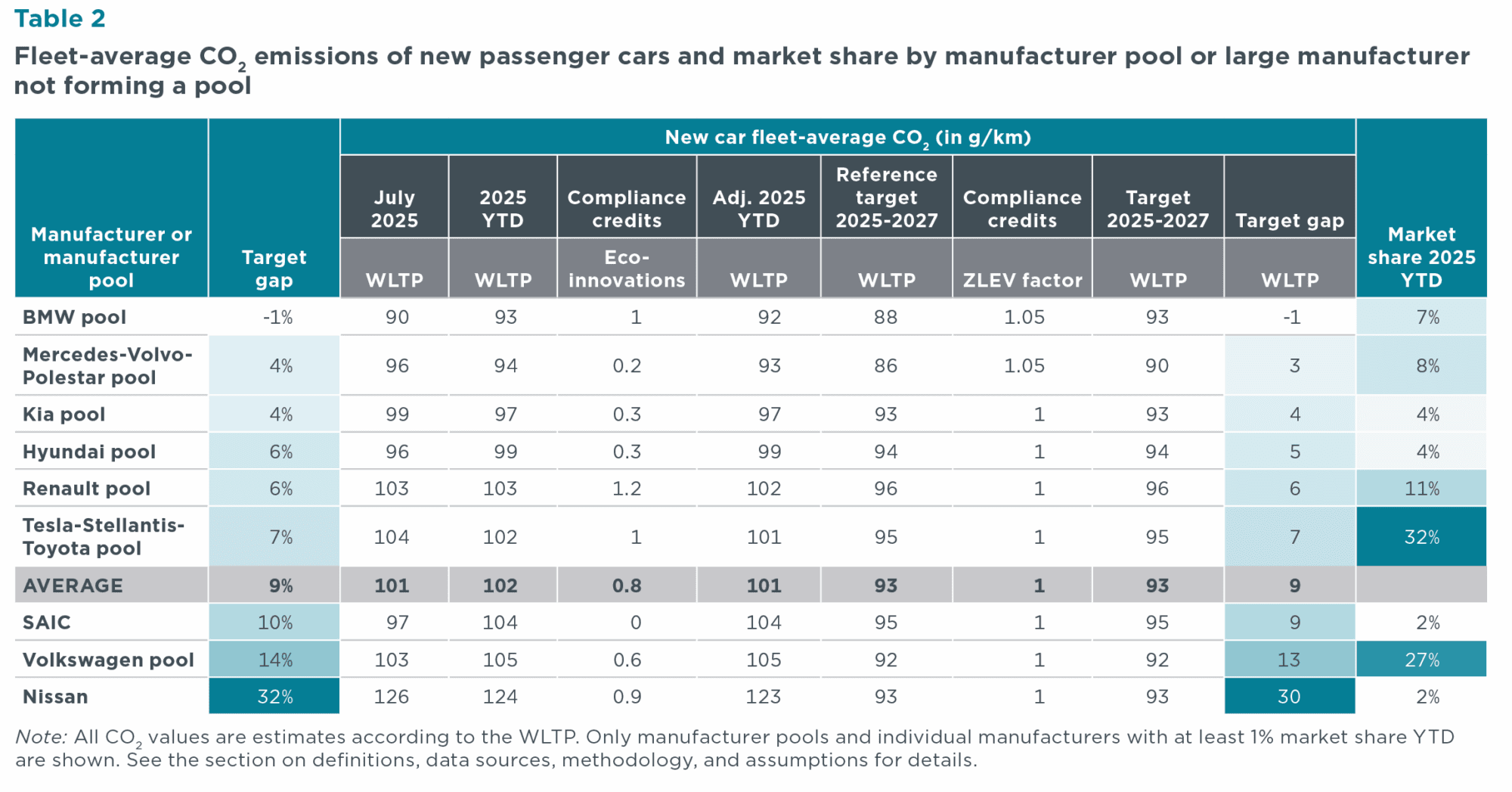

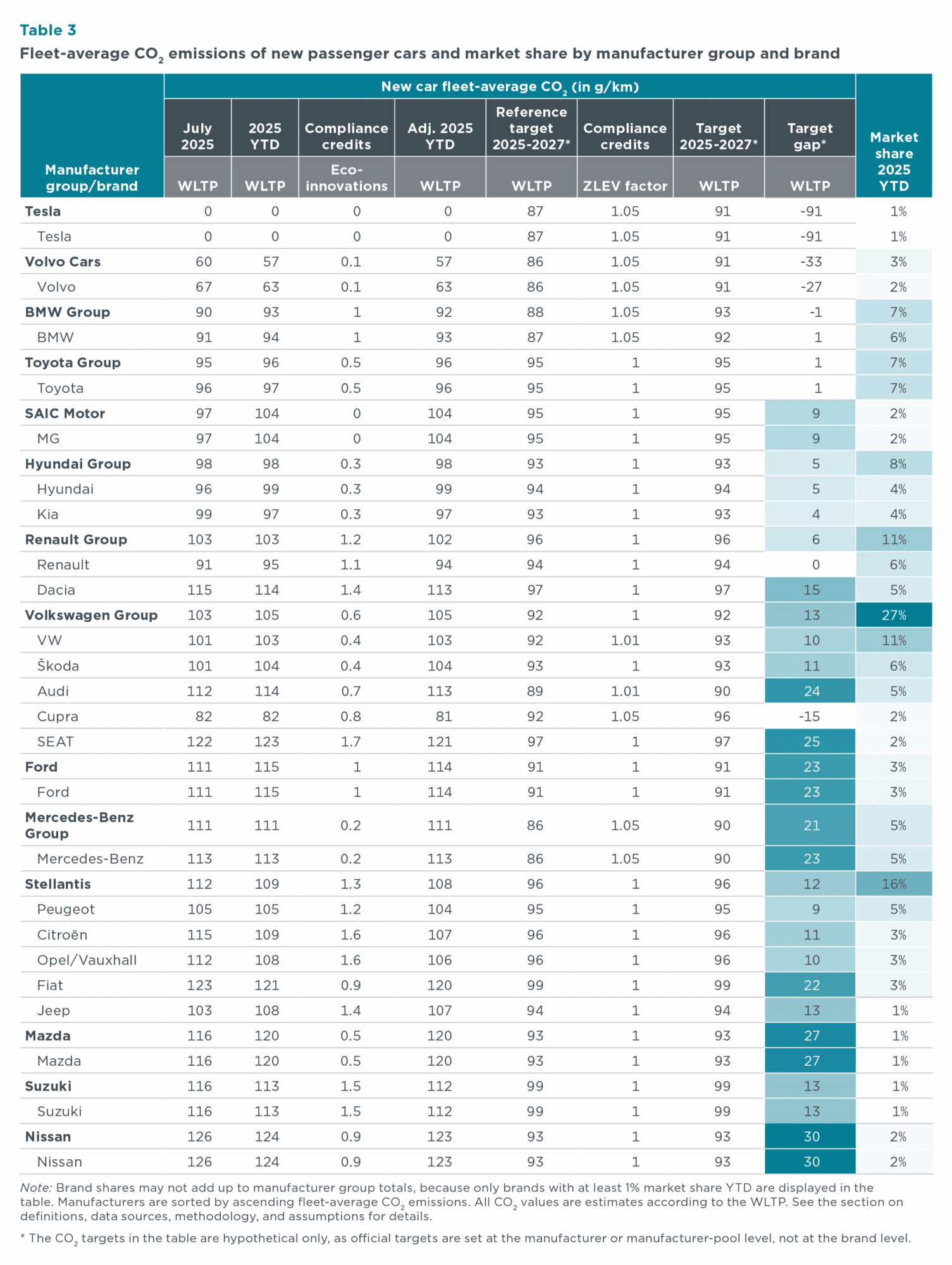

Figure 2. Average CO2 emissions of manufacturer pools and individual manufacturers compared with estimated 2025-2027 targets, 2025 YTD

Note: Includes compliance credits. All CO2 values are estimates according to the Worldwide harmonized Light vehicles Test Procedure (WLTP). Only manufacturer pools and individual manufacturers with at least 1% market share YTD are shown. See the section on definitions, data sources, methodology, and assumptions for more.

Carbon dioxide (CO2) emissions among manufacturer pools averaged 102 g CO2/km in the first seven months of 2025. Manufacturing pools thus remain 9 g CO2/km from the average target of 93 g CO2/km for the 2025–2027 period. With a market share of 32%, the Tesla-Stellantis-Toyota pool widened its target gap by 1 g CO2/km compared with the previous month. In contrast, the Mercedes-Volvo-Polestar and Hyundai pools, which together account for 12% of the market, each reduced their target gaps by 1 g/km. The BMW pool is now in compliance with its 2025–2027 target, while Nissan (30 g CO2/km above) remains the farthest behind.

Looking at individual car brands with market shares of 1% or greater, apart from Tesla, Volvo had the greatest over-compliance at 27 g CO2/km below its projected brand-level average target for 2025–2027, followed by Cupra, which was 15 g CO2/km below its target. Nissan and Mazda currently have the largest target gaps at 30 and 27 g CO2/km, respectively.

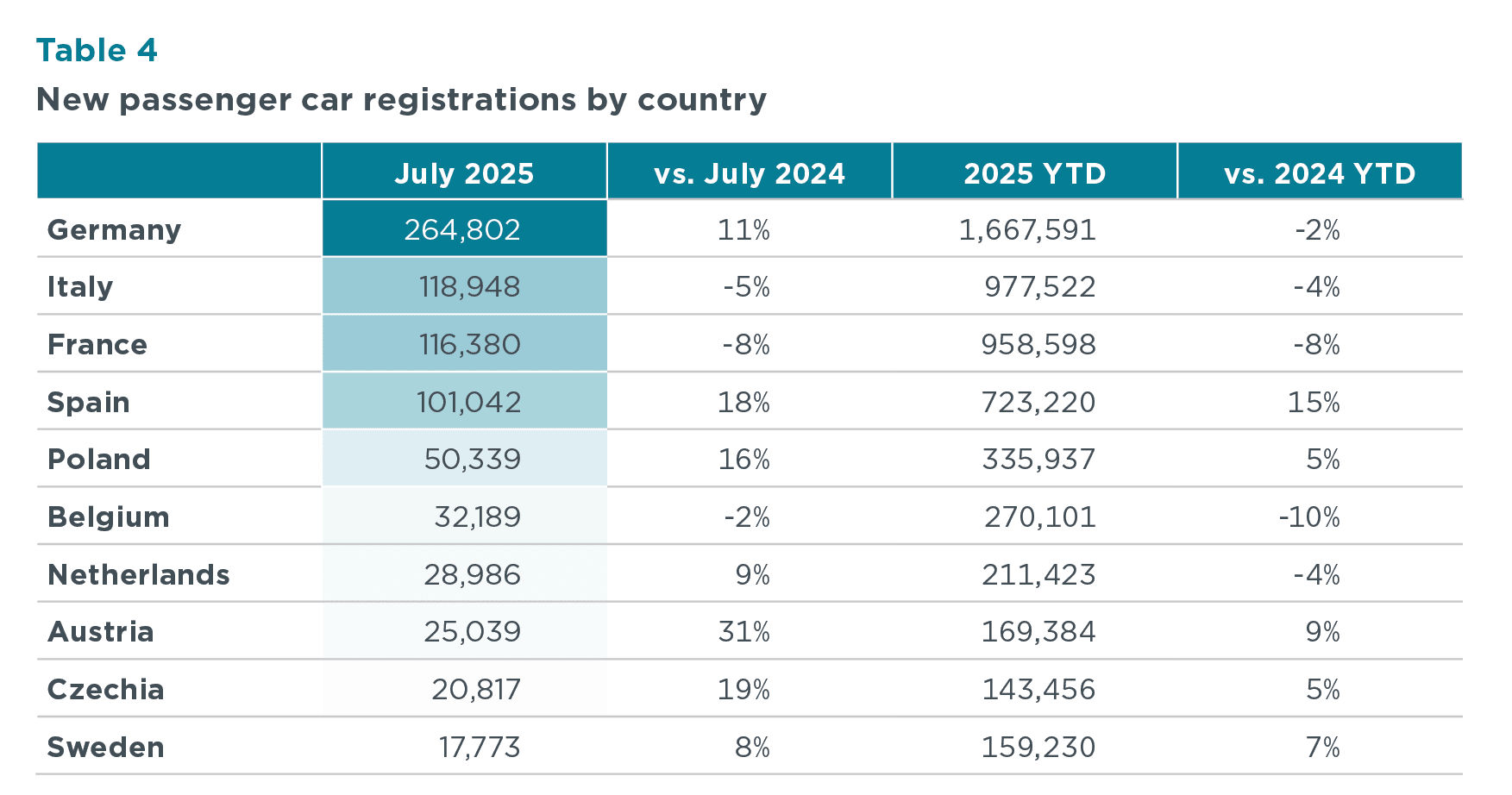

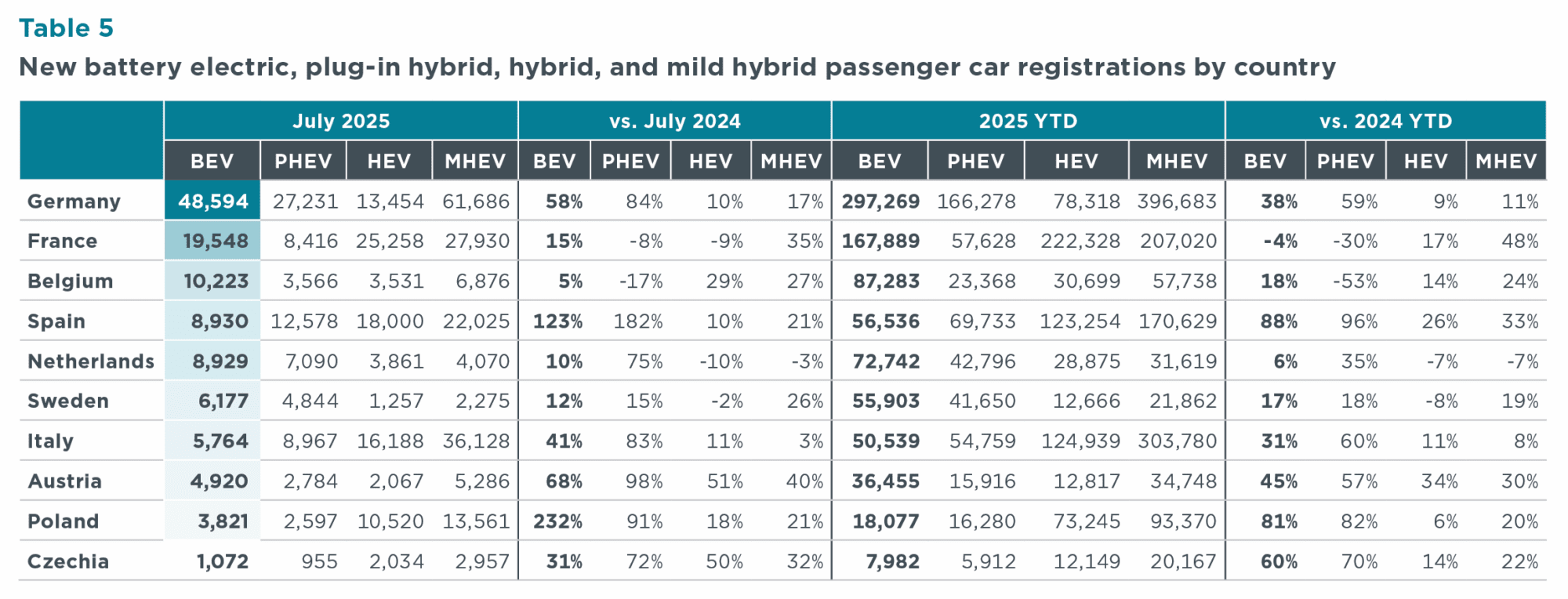

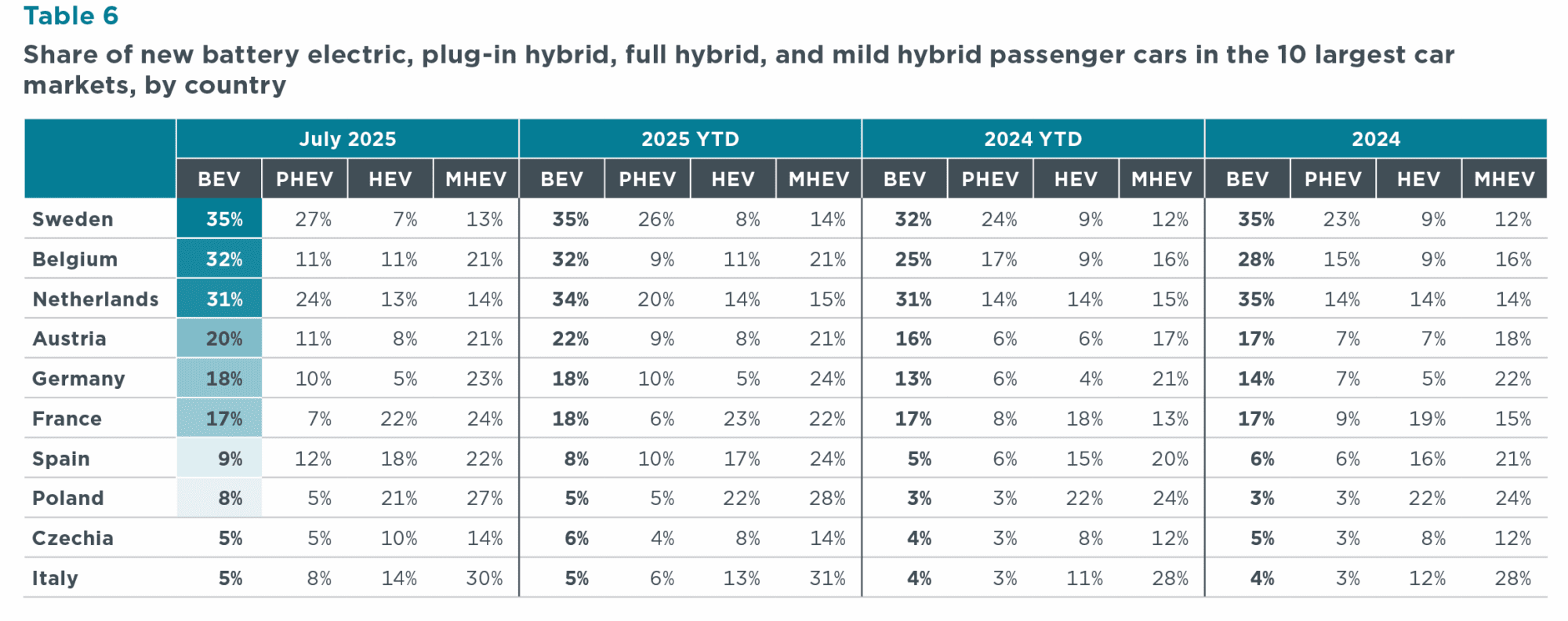

Between January and July 2025, total passenger car registrations among the major European markets grew most in Spain (+15%), Austria (+9%), and Sweden (+7%) compared with the same period in 2024. During this time, registrations declined in Belgium (-10%), France (-8%), Italy (-4%), the Netherlands (-4%), and Germany (-2%). Focusing on the largest markets by combined new BEV and PHEV registrations, Norway (96%), Denmark (67%), Sweden (61%), and the Netherlands (55%) all had combined shares above 50%. Belgium (41%), Austria (31%), and Germany (28%) also recorded combined BEV and PHEV market shares above the European average. Among the largest markets by total new passenger car registrations, BEV growth was strongest in Spain (+88%), Poland (+81%), and Czechia (+60%) in 2025 YTD compared with the same period in 2024. In France, BEV registrations fell by 4% over the same period, while Germany, the largest European market, continued to see significant growth, with BEV registrations up 38% in 2025 YTD compared with the same period in 2024 and over 48,500 units registered in July alone. Registrations of PHEVs increased the most in Spain (+96%) and Poland (+82%) in 2025 to date compared with 2024, and HEV registrations increased the most in Austria (+34%) and Spain (+26%). Shares of MHEVs were highest in Italy (31%) and Poland (28%) in 2025 to date, and they are gaining popularity in France, where registrations increased 48% in 2025 to date, compared with the same period in 2024.

Figure 3. Share of plug-in hybrid and battery electric passenger cars by country, including information on market size (total new car registrations)

Corporate fleets, comprised of company fleets (34%), car dealers and manufacturers (15%), and short-term rentals (13%), made up 61% of the total registrations in the second quarter (Q2) of 2025, while private cars made up 39% of the market. Short-term rental registrations fluctuate more than other owner types; they ranged from only 6% in Q3 2024 to nearly 13% of sales in Q2 2025. In Q2 2025, the split of new registrations by owner type largely mirrored that of Q2 2024.

Figure 4. New passenger car registrations by owner for 19 select European countries

Since 2022, France’s annual market share of BEVs among new passenger car registrations has consistently matched or slightly exceeded the European average. In the first seven months of 2025, BEVs accounted for 18% of new registrations, up 1 percentage point from the same period in 2024. Unlike other major markets such as Germany and Italy, France did not experience a decline in 2024 but instead maintained a stable BEV share of about 17%, likely supported by the social leasing scheme active in early 2024.

New car registrations by owner type in France were evenly split in 2024, with corporate fleets representing 53% of the market and private individuals representing the remaining 47%. Until the end of 2024, BEVs were much more common among private buyers than corporate fleets. In the first half of 2025, however, this gap closed as private demand weakened and fleet adoption increased, bringing BEV shares to similar levels for both groups.

The rising adoption of BEVs in corporate fleets in recent years may have been driven by fiscal measures introduced in 2023, including higher purchase and usage taxes on internal combustion vehicles and favorable tax rates for the private use of company BEVs. Additional incentives were introduced in early 2025: increased reductions to the company car benefit-in-kind tax for BEVs; a stricter CO₂ penalty scheme at the time of registration (“malus écologique”), applicable also for private registrations; and legally binding progressive annual targets for the share of low-emission vehicles in large corporate fleets, enforced by a penalty for non-compliance known as the Incentive Annual Tax. These incentives are expected to further encourage companies to transition to electric vehicles.

Conversely, private demand may have been dampened by successive reductions in the purchase bonus for BEVs (“bonus écologique”), which also applied to corporate car registrations, as well as by delays in restarting the social leasing scheme, now expected in September 2025. In July 2025, however, the ecological bonus was raised again, with higher amounts granted to lower-income households. Together with the relaunch of the social leasing scheme, this is expected to support an increase in BEV sales in the second half of 2025.

Figure 5. Share of battery electric in new passenger car registrations in France

Figure 6. Share of battery electric in new passenger car registrations in France by owner type. Source: C-Ways.

This publication is a collaboration between the ICCT, IMT-IDDRI, and ECCO think tank.

Download

European Market Monitor: Cars and vans (June 2025)

July 25, 2025

European Market Monitor: Cars and vans (May 2025)

June 25, 2025

European Market Monitor: Cars and vans (March 2025)

April 30, 2025

Join our mailing list to keep up with ICCT’s latest research and analysis.

Contact Us

We use cookies to improve site functionality and make this website more useful to visitors. Find out more.

This website uses cookies to enable some basic functionality and also to help us understand how visitors use the site, so that we can improve it.

Essential cookies provide basic core functionality, such as saving user preferences. You can disable these cookies in your browser settings.

We use Google Analytics to collect anonymous information about how visitors interact with this website and the information we provide here, so that we can improve both over the long run. For more on how we use this information please see our privacy policy.

Related Article