Market Spotlight

November 26, 2025 |

Download

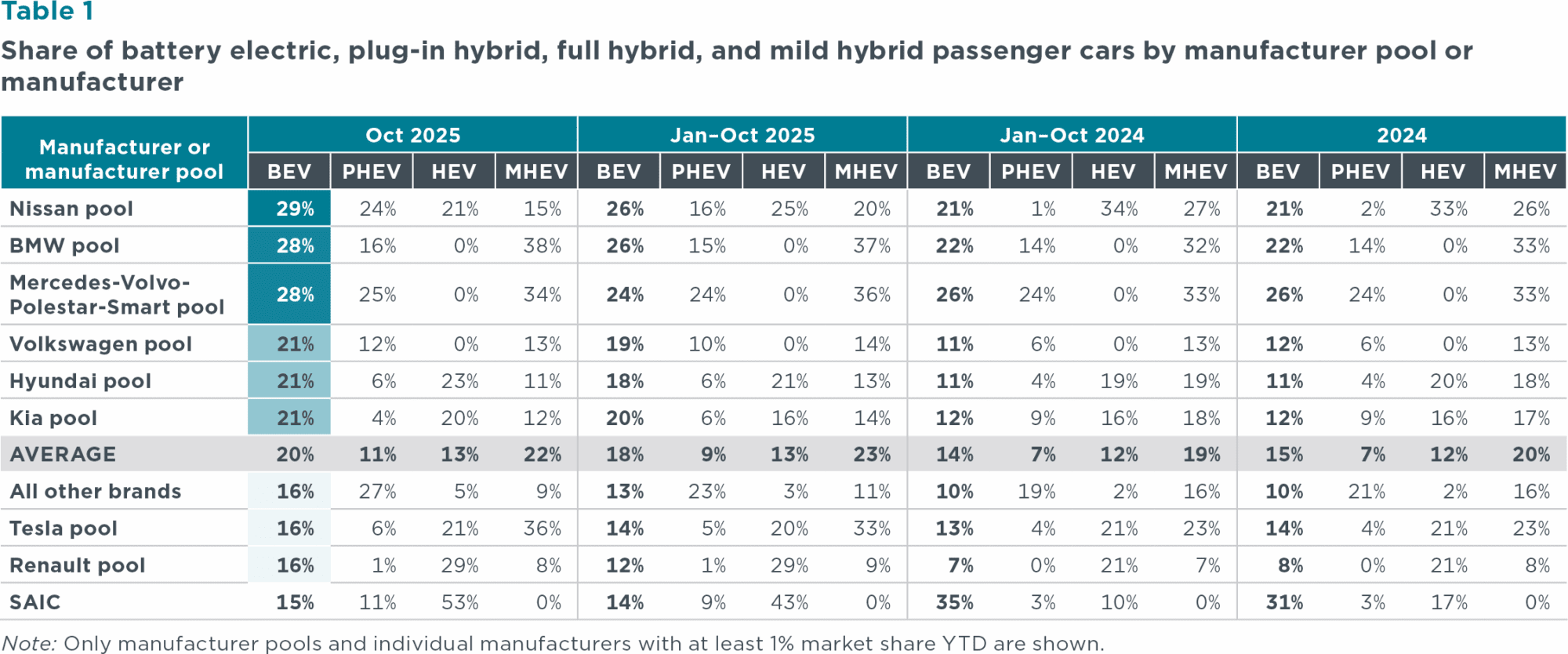

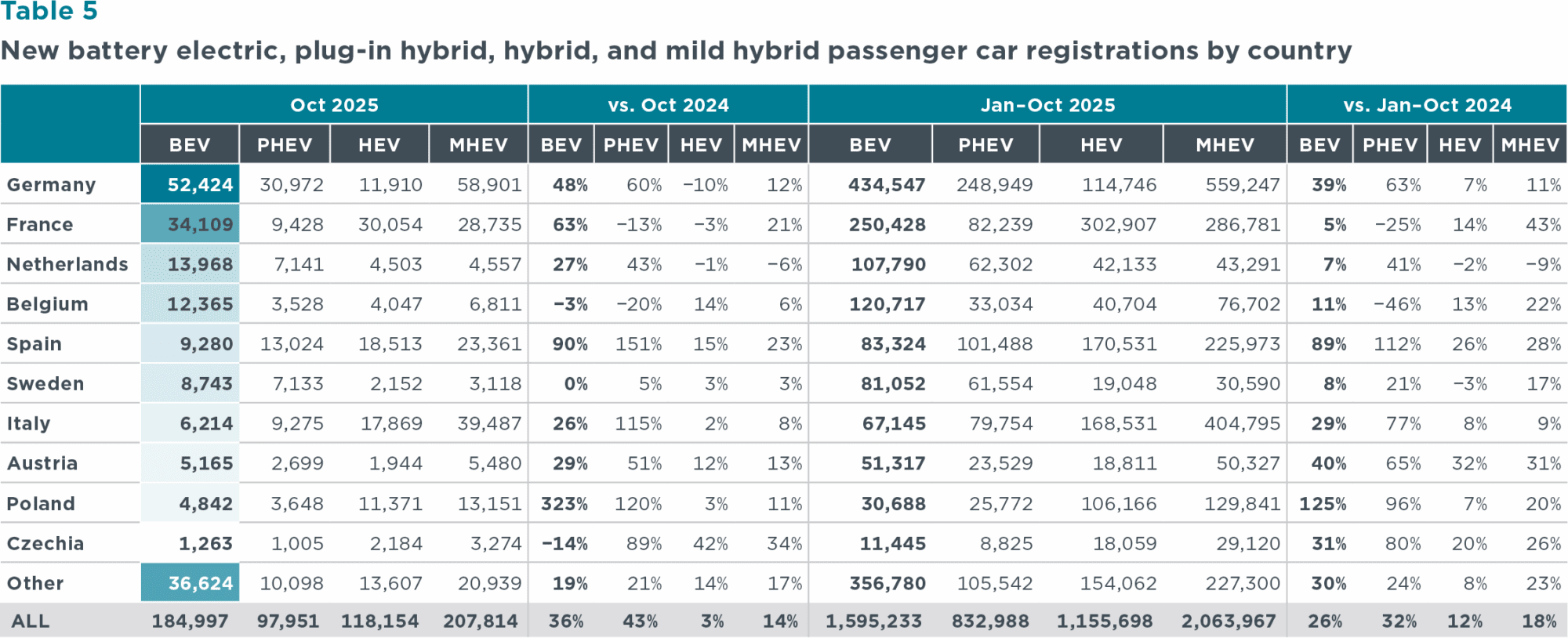

For 2025 year-to-date (YTD), the BEV share increased to 18%, which represents an increase of 4 percentage points compared with the same period in 2024. Several manufacturing pools had significant increases in BEV shares in 2025 YTD versus the same period in 2024. Kia (20%) and the Volkswagen pool (19%) each recorded an 8 percentage-point increase, while BEV shares for the Hyundai pool (18%) increased 7 percentage points. By contrast, SAIC stood out with a drop in BEV share from 35% in January–October 2024 to 14% in 2025 YTD. Plug-in hybrid electric vehicles (PHEVs) had an average market share among new registrations in Europe of 9% in 2025 YTD (up 2 percentage points over the same period in 2024), led by the Mercedes-Volvo-Polestar-Smart pool (24% share). For full hybrid electric vehicles (HEVs), SAIC (43%), the Renault pool (29%), and the Nissan pool (25%) recorded the largest shares in 2025 YTD. In the mild hybrid electric vehicle (MHEV) segment, the BMW and Mercedes-Volvo-Polestar-Smart pools led in registration shares in 2025 YTD, at 37% and 36%, respectively.

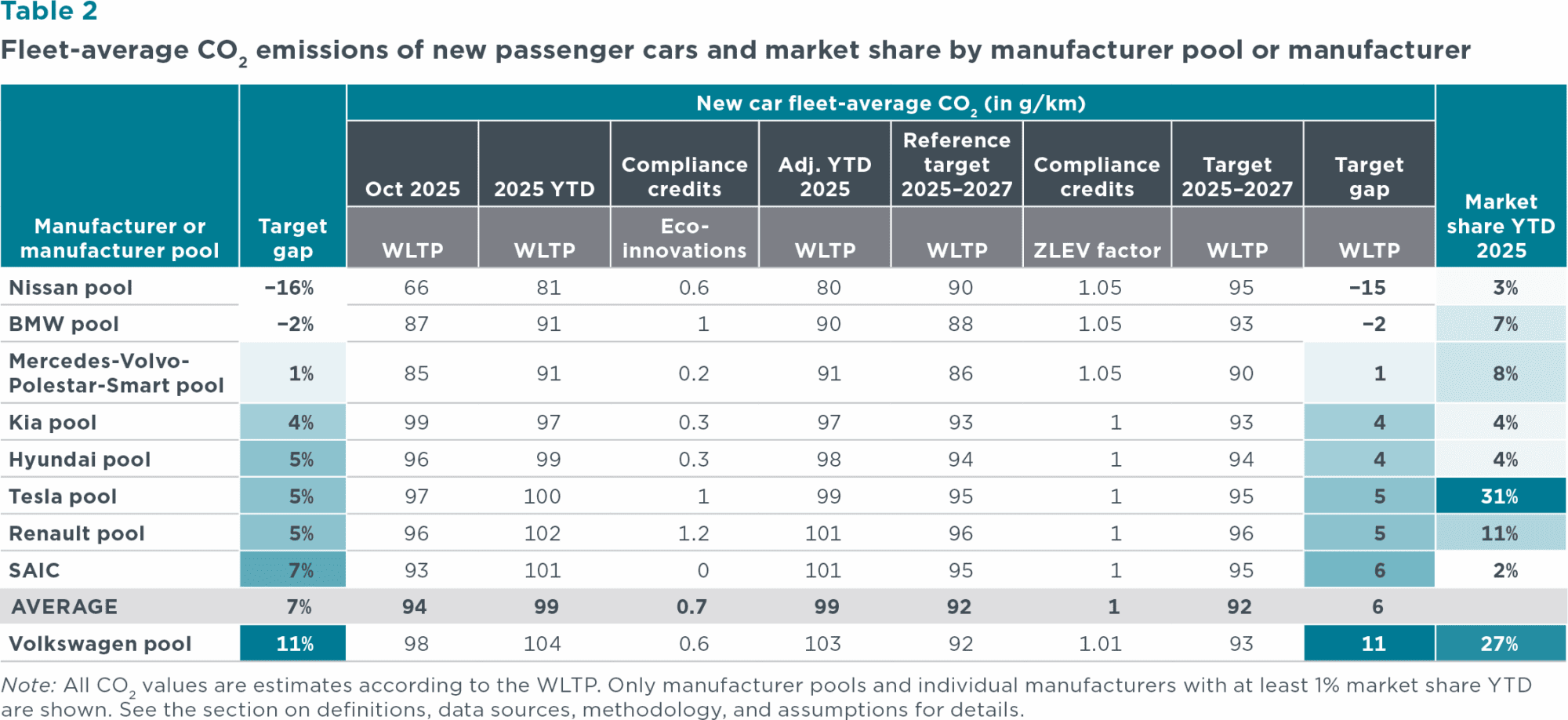

Figure 2. Average CO2 emissions of manufacturer pools and individual manufacturers compared with estimated 2025-2027 targets, 2025 YTD

Carbon dioxide (CO2) emissions among manufacturer pools averaged 99 g CO2/km in 2025 YTD. Manufacturing pools thus remain 6 g CO2/km from the average target of 92 g CO2/km for the 2025–2027 period. Compared with the previous month, nearly all of the manufacturer pools reduced their target gap by 1 g CO2/km. The newly formed Nissan pool and the BMW pool are currently in compliance with their 2025–2027 targets (15 and 2 g CO2/km below the target, respectively), while the Mercedes-Volvo-Polestar-Smart pool is 1 g CO2/km short of meeting its target. The Volkswagen pool remains the furthest behind, exceeding its target by 11 g CO2/km.

Looking at individual car brands with market shares of 1% or greater, Tesla and BYD had the greatest over-compliance at 91 and 82 g CO2/km below their projected brand-level average targets for 2025–2027, respectively, followed by Volvo (30 g CO2/km below), Mini (17 g CO2/km below) and Cupra (16 g CO2/km below). Nissan (30 g CO2/km above), SEAT (25 g CO2/km above), Mazda (22 g CO2/km above), and Audi (22 g CO2/km above) currently have the largest target gaps. Mazda reduced its target gap by 3 g CO2/km and Ford and MG reduced their target gaps by 2 g CO2/km each compared with the previous month.

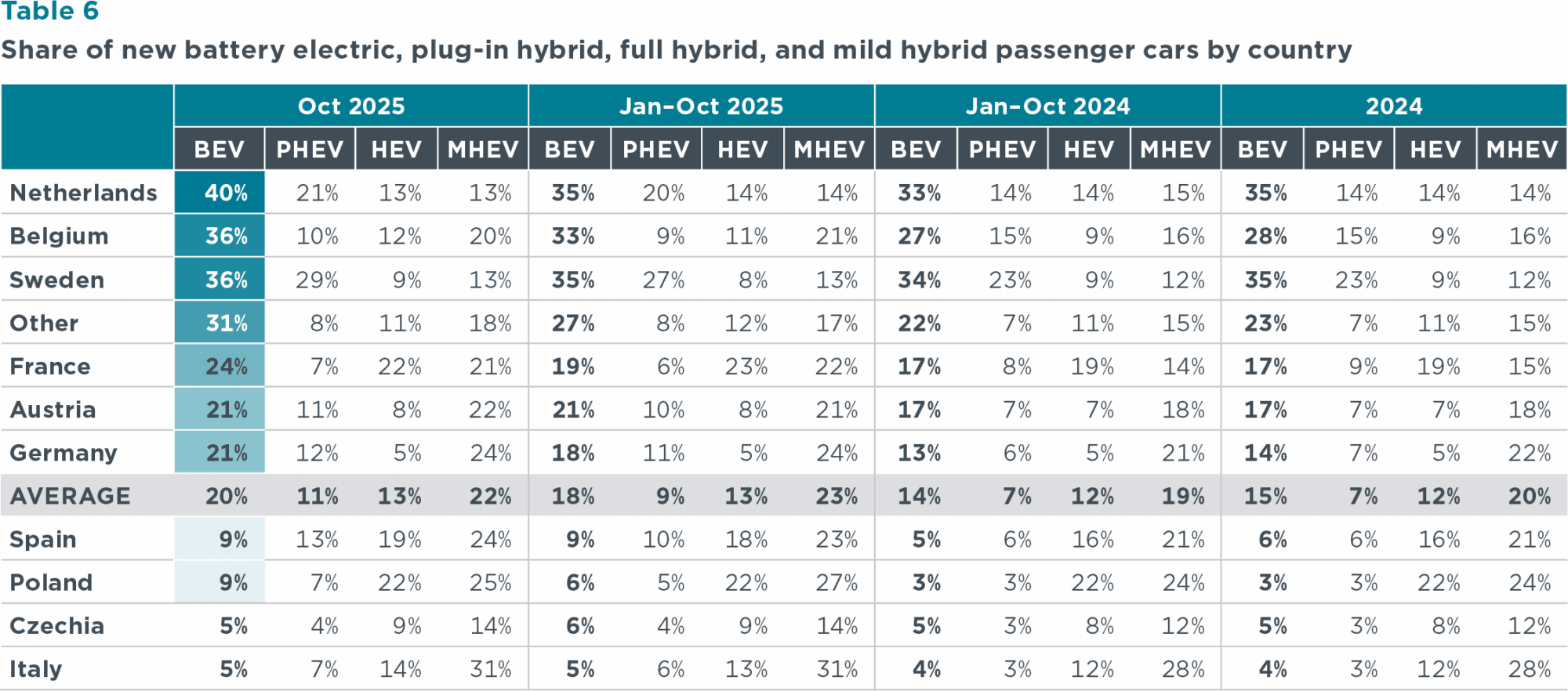

Poland, the fifth largest European market by new passenger car registrations, has seen a surge in electric vehicle (EV) uptake in 2025. Year to date, new BEV registrations more than doubled compared with the same period last year. In October 2025, BEVs accounted for 9% of new registrations, a historic high and 7 percentage points above October 2024. Year to date, the BEV market share stood at 6%, up 3 percentage points from the same period in 2024 (Figure 5). Although its BEV share remained below the European average, Poland has now surpassed other major markets—specifically Italy (the third largest) and Czechia (the 10th largest)—since the beginning of 2025.

In February 2025¾later updated in October 2025 the Polish government launched “NaszEauto” (“Our E-car”), an incentive program supporting the purchase, rental, and lease of new battery electric cars, vans, and small buses (up to 5 tonnes).1 Applications can be submitted until the end of April 2026 or until the budget of zł 1.18 billion (approximately €0.28 billion) is exhausted. Eligible beneficiaries include private individuals, self-employed individuals, and select local government entities. The base incentive is zł 30,000 (about €7,000), with additional bonuses currently available to holders of the Large Family Card and to applicants who scrap an older internal combustion engine vehicle. In total, the subsidy can be as high as zł 40,000 (about €9,500) per car. In the October revision, the bonus that was previously offered to lower income households was removed.

Since its launch, monthly “NaszEauto” applications have trended upward, reaching a total of about 19,500 submitted applications by the end of October, with 72% for leasing and 28% for direct purchase. Complementing this momentum, a range of national and European programs are supporting the expansion of Poland’s public charging infrastructure, with a particular focus on fast charging stations along the TEN-T network. By October 1, 2025, there were about 6,500 fast public and semi-public chargers installed in Poland, marking an 83% increase compared with October 1, 2024 (Figure 6).

The authors thank Aleksander Rajch from the Polish New Mobility Association (PSNM), who provided key input on policy and market developments in Poland.

Figure 6. Number of public and semi-public chargers installed in Poland by power output type and power bin

Note: Semi-public chargers are chargers located on private property that typically have access restrictions, such as specific opening and closing times. By comparison, public chargers are accessible to all people 24 hours a day, 7 days a week. AC (alternating current) chargers, often referred to as normal chargers, are slow or semi-fast chargers that deliver up to 50 kW of power in the form of alternating current from the electrical grid. By contrast, DC (direct current) chargers, or fast chargers, supply power directly to the vehicle’s battery, bypassing the onboard converter. These chargers typically supply power of 50 kW or greater, enabling faster charging.

This publication is a collaboration between the ICCT, IMT-IDDRI, and ECCO think tank.

Download

European Market Monitor: Cars and Vans (August 2025)

September 25, 2025

European Market Monitor: Cars and vans (June 2025)

July 25, 2025

European Market Monitor: Cars and vans (May 2025)

June 25, 2025

European Market Monitor: Cars and vans (March 2025)

April 30, 2025

Join our mailing list to keep up with ICCT’s latest research and analysis.

Contact Us

We use cookies to improve site functionality and make this website more useful to visitors. Find out more.

This website uses cookies to enable some basic functionality and also to help us understand how visitors use the site, so that we can improve it.

Essential cookies provide basic core functionality, such as saving user preferences. You can disable these cookies in your browser settings.

We use Google Analytics to collect anonymous information about how visitors interact with this website and the information we provide here, so that we can improve both over the long run. For more on how we use this information please see our privacy policy.